The Courage Gap

Why Oil & Gas Service Providers Struggle to Adapt — and Why Bold Strategy Is Now the Safer Bet

Editor’s note — April 2026

Brent crude recently neared USD 120 and oil & gas equities have rallied on the US–Iran conflict and the partial closure of the Strait of Hormuz. The surface read: the hydrocarbon cycle has more room to run. The deeper read is the opposite. Every major importing government — EU, Japan, Korea, India, China — is treating this spike as confirmation that Middle-East oil dependence is an unacceptable structural risk. Energy-security policy is accelerating, not pausing. The argument below holds more now.

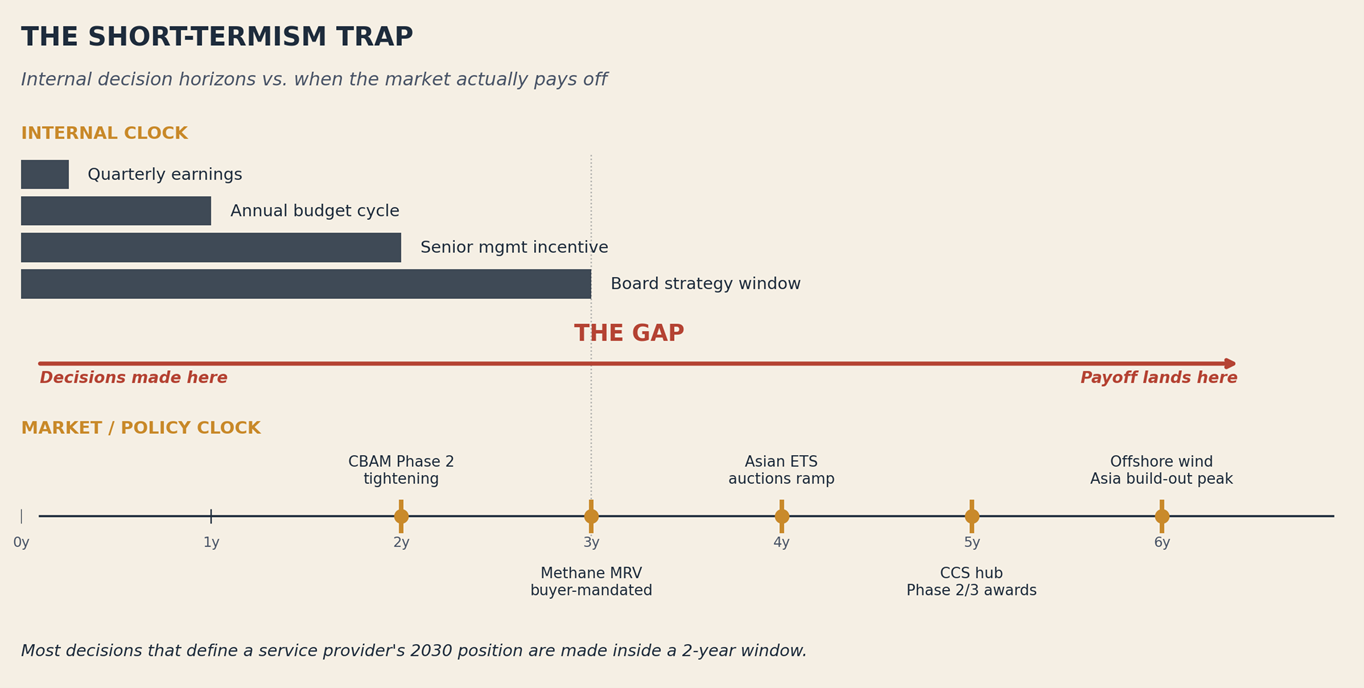

The energy transition is not being held up by technology, capital, or policy. It is being held up by a quieter problem: an industry whose internal clock runs quarterly is being asked to answer a market whose clock runs decadally.

Most senior leaders know this. Most still hesitate.

Here is why.

The hesitation has a cause, and it isn’t stupidity

No senior leader is unaware of CBAM, carbon pricing, or the CCS and offshore-wind pipeline. Intelligence is not the problem. What holds the industry back is a cultural operating system optimised for stability, not bold repositioning. Five features do most of the work.

Quarterly earnings culture. A CCS pilot eating USD 40m of capex is hard to defend on an earnings call against a drilling program running at a 25 percent margin.

Capital intensity magnifies the incumbent asset. When the balance sheet is dominated by rig fleets, fabrication yards or vessels, every strategic decision starts from “how do we keep these assets earning.” That framing quietly narrows the option set.

Engineering culture rewards technical conservatism. The discipline that keeps the industry safe at scale defaults to “prove it first” a culture that translates poorly to betting on markets that do not yet exist at scale. Firms that wait for proof become customers of the firms that didn’t.

Backlog-based planning is backward-looking. A three-year plan built from signed contracts cannot contain a market that has not opened yet.

Incentive systems run on 12–18-month metrics. Decisions whose payoff sits in 2029–2030 are made by people whose personal economics end well before then.

The cost of waiting is no longer theoretical

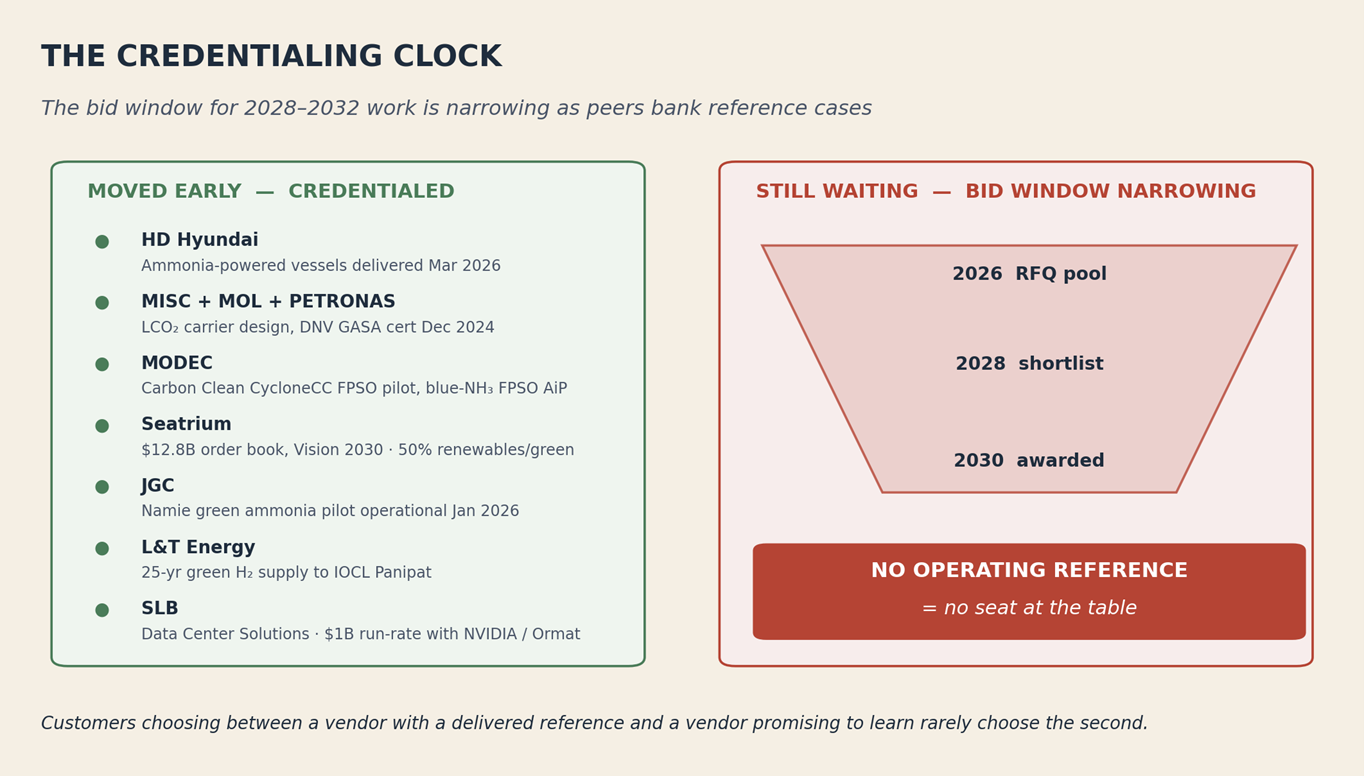

Until recently, the cost of hesitation was abstract. Today, it is showing up in signed contracts and capability gaps.

PETRONAS’s Kasawari CCS is pulling first injection forward to 2027 at 3.3 Mt/yr. Providers without an operating reference by 2028 will struggle to bid on Phase 2 and 3.

JERA and KOGAS co-founded the CLEAN coalition. Early methane-MRV vendors become defaults when buyer-mandated differentiation arrives.

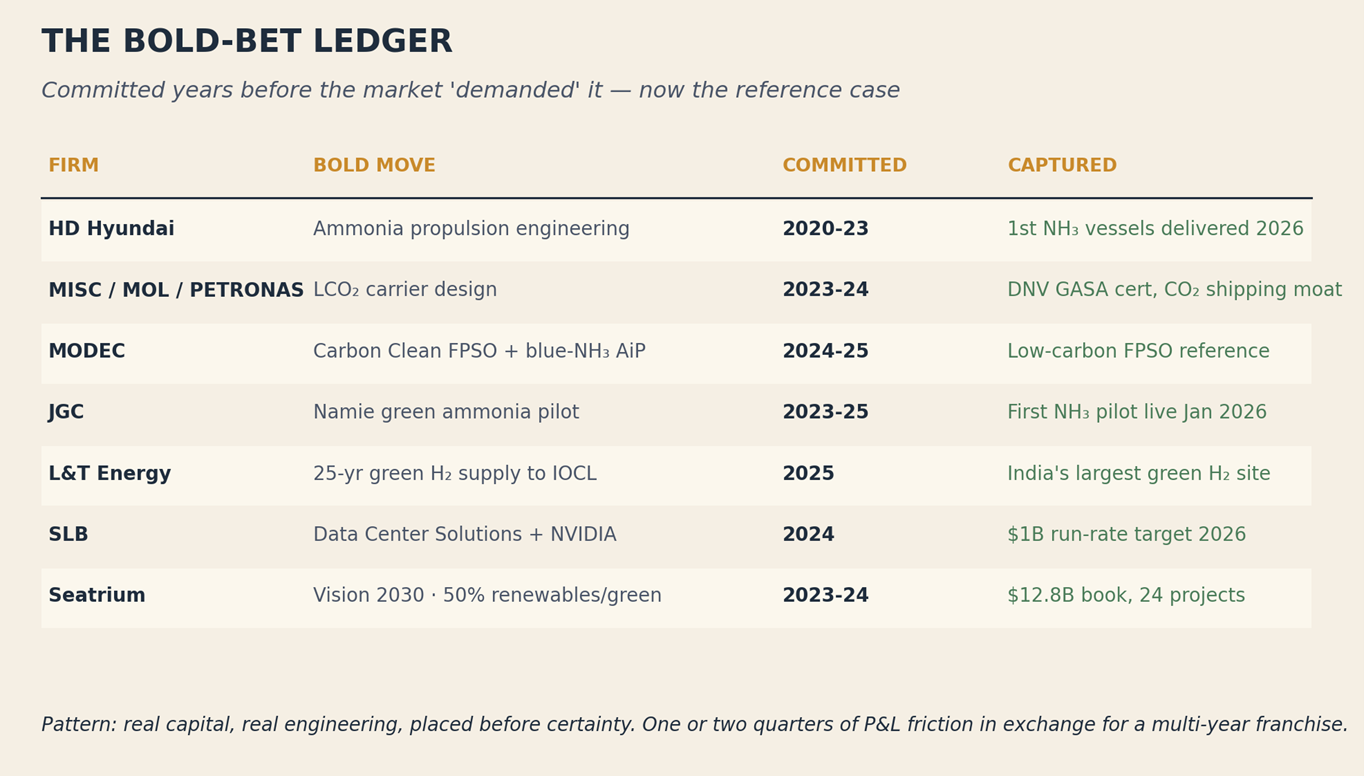

HD Hyundai delivered the world’s first ammonia-powered commercial vessels — Antwerpen and Arlon — in March 2026.

MISC, MOL and PETRONAS won DNV GASA certification for liquid-CO₂ carrier designs in December 2024; MISC’s MMEGA-class FPSO cuts CO₂ per barrel by 40 percent.

Seatrium’s order book hit USD 12.8 billion in Q3 2025 across 24 projects through 2031.

These are not pilots, they are firms whose commercial positioning for 2028–2032 is already locked in.

What bold actually looks like

Bold does not mean reckless. It means committing real capital, leadership and engineering depth to a market category before it is safe to do so.

HD Hyundai committed years of engineering to ammonia propulsion before the first customer existed.

MODEC signed an AiP for a blue-ammonia FPSO and a CycloneCC pilot aimed at 100,000 t/yr CO₂ capture on an operating FPSO — a scale nobody has validated yet.

JGC opened the Namie green ammonia pilot in January 2026.

L&T Energy is building India’s largest green hydrogen plant at IOCL Panipat under a 25-year contract.

SLB is two years into Data Center Solutions, targeting a USD 1 billion run-rate with NVIDIA and Ormat.

None of these firms had certainty. They had conviction.

The asymmetry has reversed

For most of the last decade, a bold new-category bet had unlimited downside while staying the course had bounded downside.

That asymmetry has flipped.

The downside of a credible bold bet is now contained — a 2–5 percent capex reallocation, a ringfenced team, a single pilot. The downside of staying the course is structural: entire market categories the firm is credentialed out of, customers migrating to peers who can transact on CBAM or Asian ETS exposure, a shareholder narrative that reads as decline.

Three bold plays

1. Place one genuinely asymmetric bet.

In CCS, ammonia, hydrogen, or offshore-wind installation — something that produces a credentialed operating reference by 2028. This decision separates the peer list above from those still waiting.

2. Stand up a small ‘2030 team’.

Reporting to the CEO, with its own P&L discipline but freedom from the standard bid-review calendar and short-term reporting cycle. Every firm on the peer list has some version of this.

3. Rebuild incentive design at the senior management layer.

Tie long-term incentive compensation to new-category revenue and credentialed references, not to backlog. Until the compensation shifts, the behaviour will not.

The takeaway

The firm that looks bold in 2026 will look prudent in 2029.

The firm that looks prudent in 2026 - protecting margin, waiting for clarity, running the backlog will look captured in 2031. The carbon rulebooks in Brussels, Seoul, Singapore and Delhi are not waiting; the customers are not either. The safer bet is no longer the cautious one — it is the bold one, sanctioned from the top.

A note on where the work actually gets stuck

The hesitation is not an analytical problem — the data is on the table. The difficulty is that the conversation has to happen among people with real incentives. The engineer who built the revenue base is asked to cannibalise it; the commercial lead whose bonus depends on this year’s backlog is asked to redirect capital to a 2030 payoff. The function head whose team would shrink under a portfolio shift is the one whose endorsement the CEO needs. These are human conflicts, and they are hard to resolve from inside. For leadership teams navigating this shift, the challenge is rarely identifying the opportunity—it is creating the internal conditions to act on it.

Helios Energy Advisory partners with oil & gas service providers on strategy, capability allocation, and the internal changes required to act on bold ideas. www.heliosenergyadvisory.com